What The Situation In Turkey Can Teach Us? (Mises Submission on 15-Feb-2022)

- R. S. Koçyiğit

- Feb 15, 2022

- 4 min read

This article was originally written and submitted to the Mises Institute on 15 February 2022, but it was not published later on. It is therefore best read as an older piece written in a specific macroeconomic context, when the inflation debate was still unfolding. In retrospect, its main argument concerning Turkey's low-interest-rate policy mix, rapid monetary expansion, and the risk of persistent inflation held up reasonably well in broad terms. Thus, in a way, I was able to predict the potential effects quite well, and one can argue that I undershoot.

At the same time, its conditional warnings to advanced economies held up well too, especially since many Western central banks tightened policy relatively quickly thereafter. I am finally publishing it after 4 years, I hope it will be a good read. And I would like to thank again so much for Roger Garrison on helping me for sources needed for this article. I hope he is resting in peace. He was indeed a legendary economist.

-R. S. Kocyigit on 28/3/2026

15th of February 2022: Meanwhile, while much of the world has been dealing with the pandemic and high inflation, Turkey has also faced a severe macroeconomic adjustment. Once frequently cited as a notable emerging-market case, the country has in recent years experienced substantial inflation, currency pressure, and broader economic instability.

A prominent policy view within the Turkish administration has emphasized the idea that lower interest rates can support growth and, in some formulations, help reduce inflation by lowering borrowing costs. This view has been widely criticized by many economists and market participants.

Turkey's GDP per capita growth between 2002 and 2013 was strong. After 2013, however, performance weakened noticeably, and on some measures real gains became much less impressive once inflation and exchange-rate effects are taken into account.[1][2]

The key question is what drove this deterioration. The data cited below suggest that a combination of negative real interest rates and rapid monetary expansion may have played an important role.[3][4]

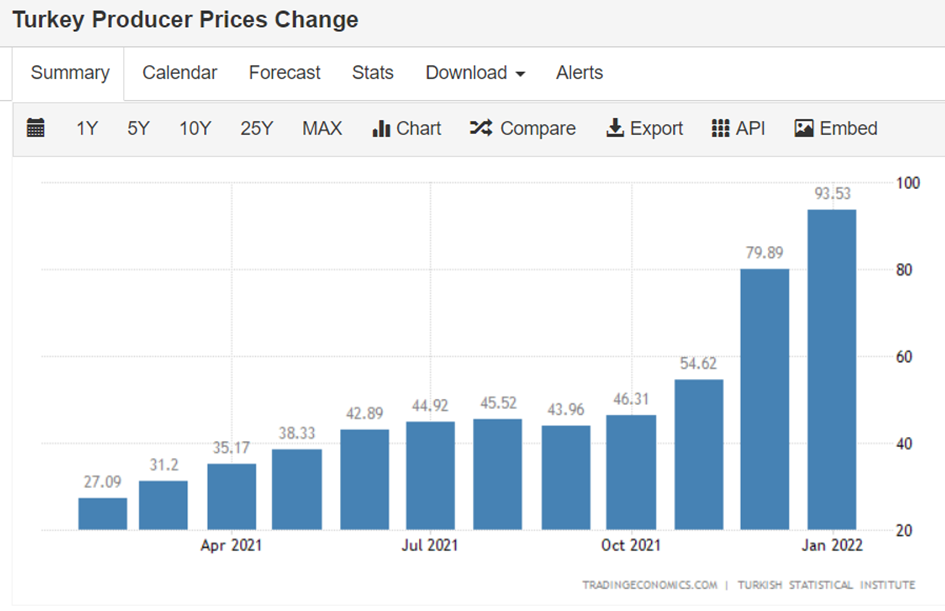

Political factors may also have mattered, but the macroeconomic dimension is central. Real interest rates averaged around -3% between 2012 and 2018. After fluctuations in 2018, they again turned deeply negative. During the pandemic period, and amid central-bank measures intended to cushion the shock, real rates fell much further. Producer prices also rose faster than consumer prices for a time, creating a notable gap between PPI and CPI.[5] Some commentators have additionally raised questions about data quality and institutional independence, though those concerns remain part of a broader public debate.

Before turning to the macroeconomic consequences of these low-rate and liquidity-expansion policies, it is useful to consider money-supply growth. Economists often use M2 as an indicator of monetary expansion. In the United States, M2 rose by roughly 40% from the beginning of the pandemic over the period referenced here. In Turkey, by contrast, M2 approximately doubled, as the charts below indicate.[6][7]

Taken together, these data are consistent with a substantial period of monetary expansion. It is therefore worth examining several possible consequences of that policy mix.

One area often discussed is the Turkish real-estate market. In Istanbul, price-to-rent ratios in some areas became extremely elevated, and annual real-estate price growth was also very high in 2021.

One possible explanation is the large role of state-owned banks in mortgage lending, which reportedly accounted for more than 60% of such lending during the period referenced here.[8]

Critics argued that pressure for lower borrowing costs was transmitted unevenly across the banking system: private banks were more reluctant to cut rates, while state-owned banks absorbed more of the adjustment. This may also have affected bank profitability.

At the same time, unemployment remained elevated. The headline unemployment rate was around 11%, while youth unemployment exceeded 20%. Some analysts also pointed to the relatively low employment rate as a reason to interpret headline labor-market data cautiously.[9][10]

On this reading, Turkey appeared to be facing a form of stagflation: weak labor-market conditions alongside high inflation. That pattern sits uneasily with simplistic interpretations of the Phillips Curve and has encouraged renewed debate about how well older macroeconomic frameworks fit current conditions.

Turkey's experience may also be relevant to broader international debates about prolonged low interest rates and large-scale monetary expansion. As Ludwig von Mises wrote in Human Action (1949), "All present-day governments are fanatically committed to an easy money policy..." For critics of expansionary monetary policy, Turkey offers a case study often cited as a warning.

The Czech Republic responded to rising inflation by increasing interest rates relatively quickly, while other Western central banks moved more cautiously during the period discussed here. Early in the inflation surge, some Federal Reserve officials suggested that inflationary pressures would be temporary. Yet producer-price inflation later reached unusually high levels by historical standards.[11]

If central banks delay adjustment for too long, critics argue that the risk of persistent inflation and asset-market distortions increases. From that perspective, Turkey's recent experience can be read as a cautionary example in debates over low interest rates, rapid money growth, and inflation management.

Sources :

[4]

[8] https://www.sozcu.com.tr/2021/ekonomi/konut-kredilerinde-kamu-ile-ozel-arasinda-buyuk-fark-6545655/

[9]

[10]

Comments